Did Fundata A+ Wins for Five Funds Just Shift National Bank of Canada’s (TSX:NA) Investment Narrative?

Investment Narrative?")

- National Bank Investments Inc., a subsidiary of National Bank of Canada, recently announced that five of its mutual funds and ETFs earned Fundata 2025 FundGrade A+ Awards for consistently strong performance in 2025.

- This recognition highlights the bank’s asset management capabilities and reinforces how its fund platforms contribute to the broader institution’s appeal for Canadian investors.

- We’ll now examine how this recognition for consistently high-performing funds shapes National Bank of Canada’s broader investment narrative and growth ambitions.

Uncover the next big thing with 10 elite penny stocks that balance risk and reward.

What Is National Bank of Canada’s Investment Narrative?

For National Bank of Canada, the core thesis still starts with believing in a diversified, domestically anchored bank that can translate stable earnings, disciplined capital returns and solid risk management into durable shareholder value. Recent Fundata A+ recognition for several NBI mutual funds and ETFs adds a fresh, if incremental, angle to that story by underscoring the bank’s asset management capabilities and its appeal to investors looking beyond pure deposit and lending products. In the near term, the more important catalysts remain credit quality trends, housing market conditions and management’s stance on dividends and buybacks, especially after recent share repurchases and dividend increases. The award news itself is unlikely to move the needle financially in the short run, but it does support the narrative that fee-based wealth and fund platforms can help balance out more cyclical pressures in lending and capital markets.

However, investors should also keep a close eye on credit risk and the relatively low bad-loan allowance.

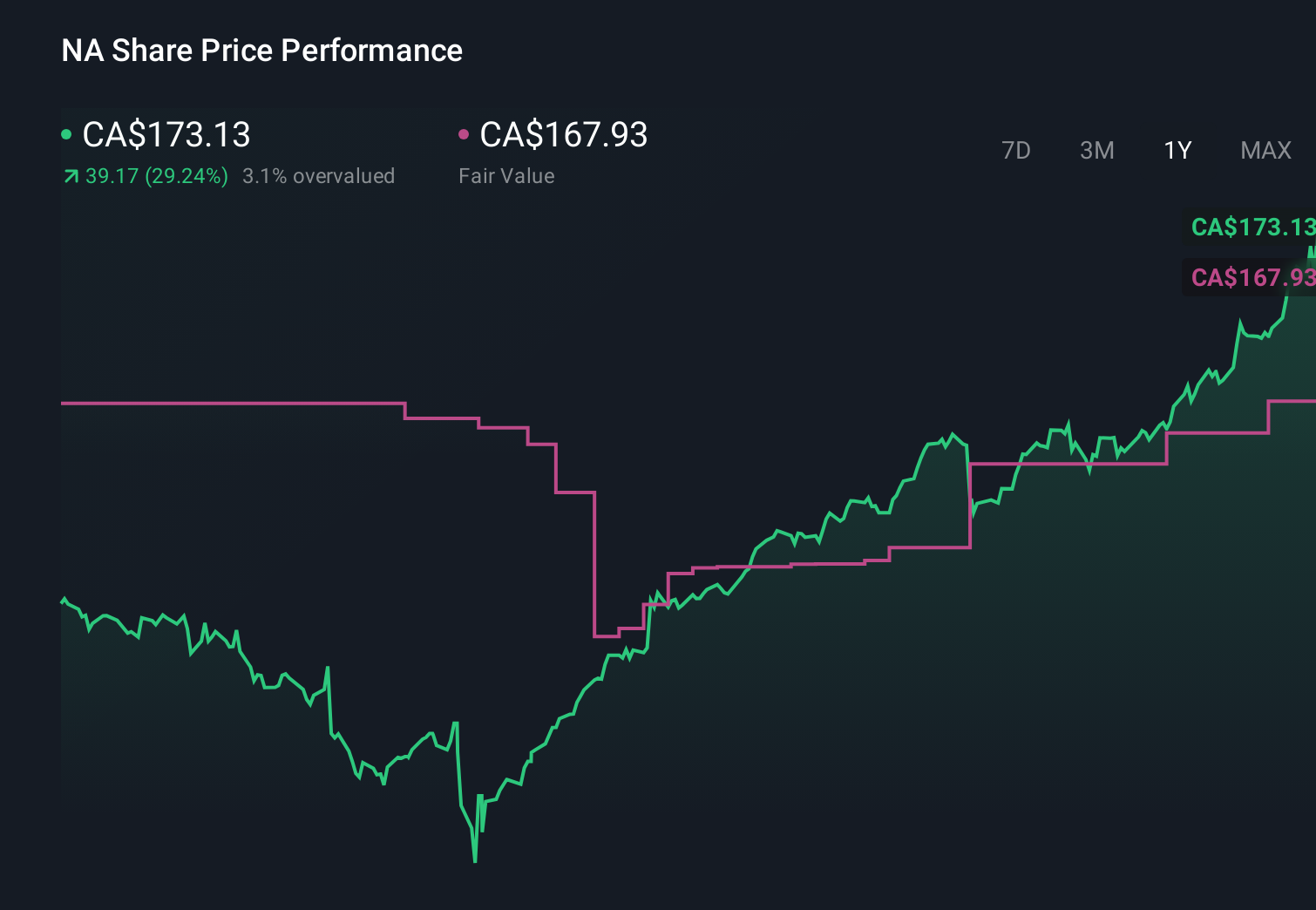

National Bank of Canada’s shares have been on the rise but are still potentially undervalued by 32%. Find out what it’s worth.

Exploring Other Perspectives

Three Simply Wall St Community fair value estimates for National Bank of Canada span from about CA$152.65 to CA$246.96, showing how far apart individual views can be. Set that against the current focus on housing-market softness, credit quality, and capital returns, and you can see why it pays to compare several perspectives before deciding how the bank might fit into your portfolio.

Explore 3 other fair value estimates on National Bank of Canada – why the stock might be worth 10% less than the current price!

Build Your Own National Bank of Canada Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes – extraordinary investment returns rarely come from following the herd.

Looking For Alternative Opportunities?

Don’t miss your shot at the next 10-bagger. Our latest stock picks just dropped:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if National Bank of Canada might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free Analysis

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

link

– News and Events")