Trump, Harris Corporate Tax Proposals: Election 2024

Depending on the outcome of the 2024 US election, the current corporate taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities.

rate of 21 percent could be in for a change. The 21 percent rate, put in place by the 2017 tax reform, brought the US rate in line with other industrialized countries after years of being the highest. The tug-of-war over where to take the corporate tax rate has significant implications for businesses planning their future domestic investments, adding uncertainty in the near term and affecting the viability of projects in the long term.

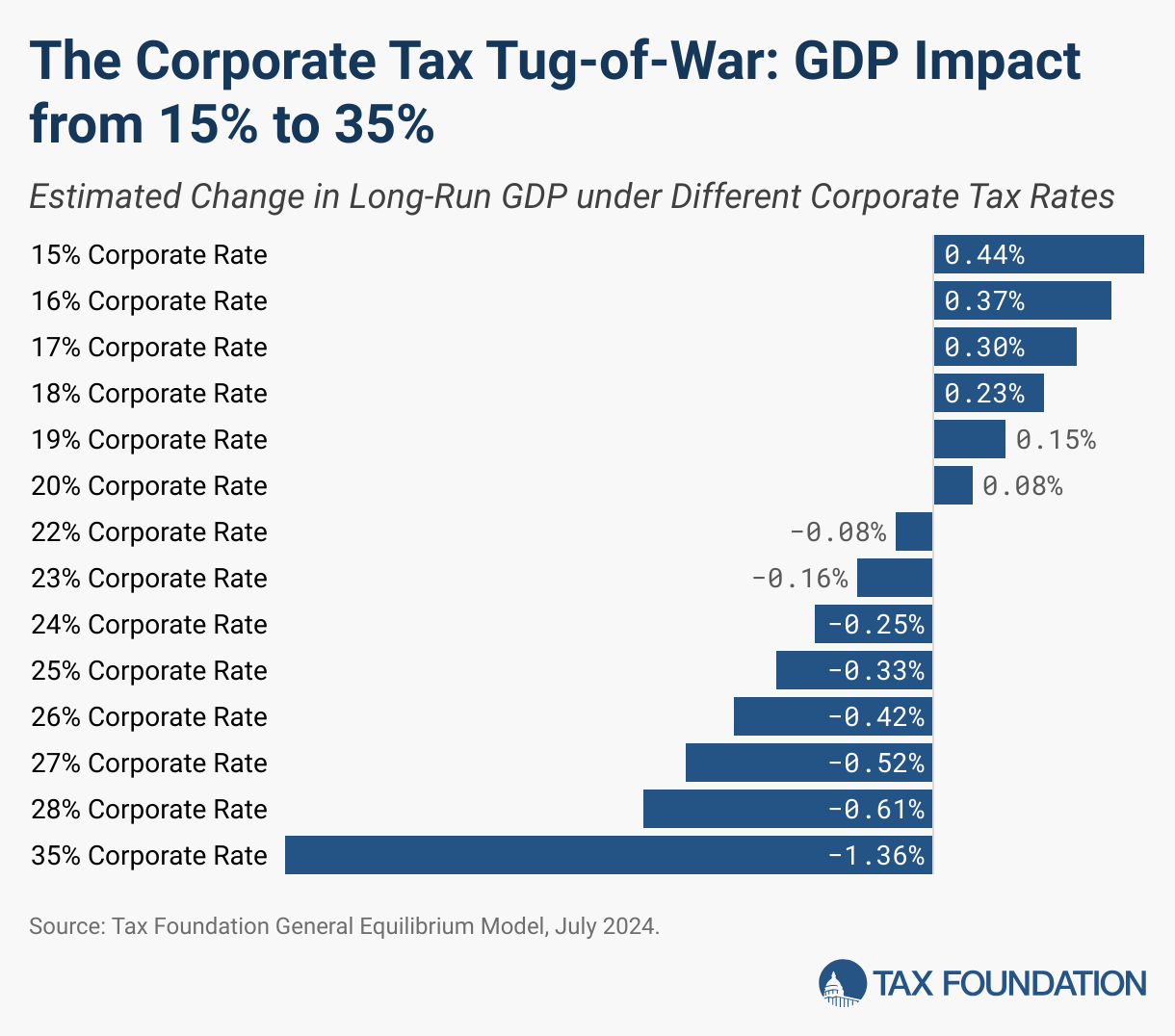

The rates under consideration by former President Donald Trump (20 percent or 15 percent) and current Vice President Kamala Harris (28 percent now, but previously as high as 35 percent) would have vastly different effects on the economy.

Using Tax Foundation’s General Equilibrium Model, we estimate that at the most extreme end, raising the corporate tax rate to 35 percent would shrink the US economy by nearly 1.4 percent and employment by 289,000 jobs. It would raise $2.2 trillion on a conventional basis, shrinking to $1.6 trillion on a dynamic basis, which factors in how a smaller economy with smaller incomes would shrink other tax revenues.

At the other end of the spectrum, lowering the rate to 15 percent would grow the US economy by slightly more than 0.4 percent. It would reduce revenue by $673 billion on a conventional basis, and by $459 billion on a dynamic basis, factoring in how the larger economy and larger incomes would grow other tax revenues.

The next president will face tough choices and trade-offs for tax policy, both because the individual provisions of the 2017 tax reform are scheduled to expire after 2025 (and full extension would reduce revenue by more than $4 trillion) and because the federal budget is already on an unsustainable path before considering $4 trillion of tax cuts. But the need for more revenue is not a free pass to impose the most damaging types of tax hikes.

Studies have shown that the corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax.

is the most harmful tax for economic growth, and recent analyses are now confirming the benefits of reducing the corporate income tax, finding that the TCJA’s corporate tax reforms significantly boosted domestic investment.

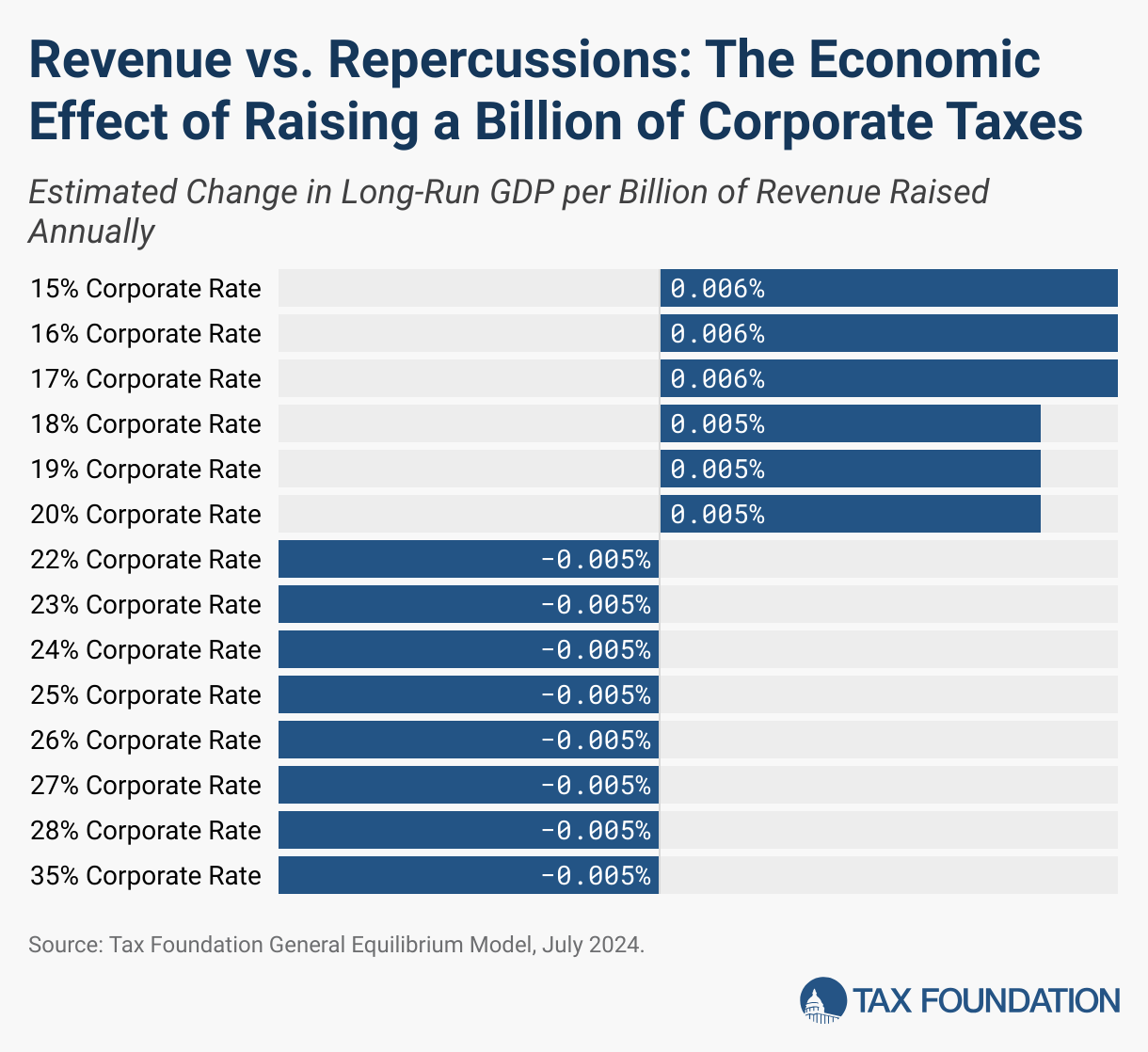

One key result from our modeling is that the “damage per dollar” of raising the corporate rate is just as significant for a small rate increase as it is for a large rate increase. The nearby chart illustrates how for every billion of revenue raised, a higher corporate rate reduces economic output by roughly the same amount. While the percentages in the chart might look small, they add up to the total economic effects shown in the first chart, and they apply to the total size of the US economy—currently measuring at $28.6 trillion.

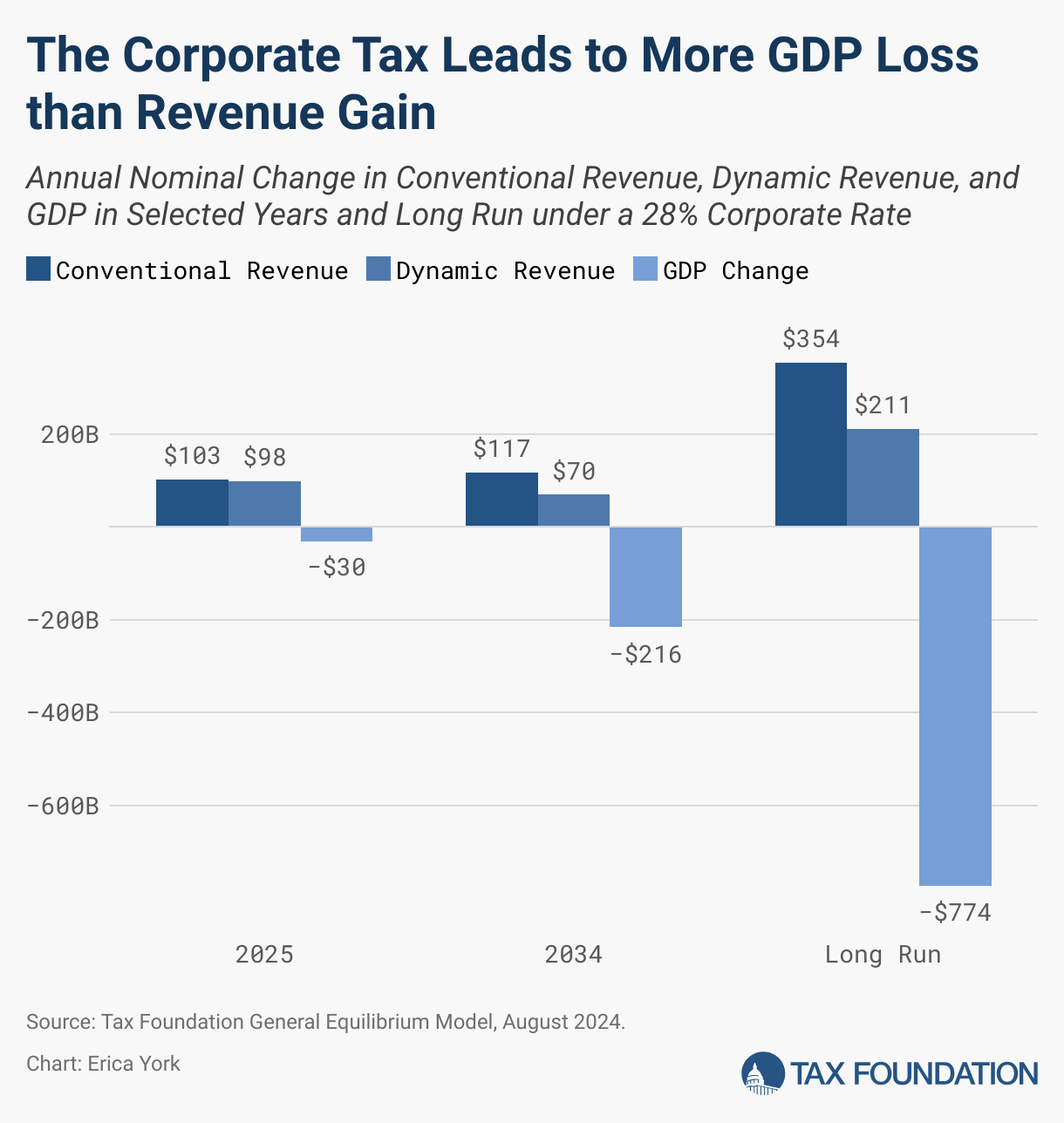

A higher corporate tax rate would raise revenue; however, any revenue would come at a high price of lost economic output, investment, and wage growth. For example, under a 28 percent corporate rate, we estimate that by 2034, for every $1 of higher revenue on a conventional basis, GDP would fall by $1.84. In the long run, when the economic effect of that higher rate fully phases in, we estimate an even steeper drop in GDP of $2.19 for every dollar raised.

Rather than turn to one of the most economically damaging tax increases, lawmakers should eliminate wasteful tax expenditures and broaden the tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates.

to raise revenue.

Conversely, while lowering the corporate tax rate would be pro-growth, the revenue loss for a lower rate should not squeeze out other pro-growth reforms to the business tax base, namely, expensing for research and development (R&D) and capital investment.

The TCJA successfully lowered the corporate rate permanently and made the US a much more attractive location for investment. At 21 percent, the US corporate tax rate now stands at about the average among industrialized countries. Further changes to corporate taxes should likewise focus on improving incentives to invest and innovate, which rules out a higher corporate tax rate for raising revenue and is best accomplished by cost recoveryCost recovery is the ability of businesses to recover (deduct) the costs of their investments. It plays an important role in defining a business’ tax base and can impact investment decisions. When businesses cannot fully deduct capital expenditures, they spend less on capital, which reduces worker’s productivity and wages.

improvements.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe

Share

link